As a rule, Republican policymakers believe corporate leaders, captains of industry, and private-sector “job creators” should get exactly what they want from politicians. After all, the GOP argues, business leaders are the backbone of the American economy and the free-enterprise system. If they have a request, it should be honored.

With this in mind, it’s fascinating to see Republicans’ Big Business allies telling their political allies not to screw around again with the debt ceiling.

The Treasury Department says the government will reach its $16.4 trillion borrowing limit by the end of the year. But “extraordinary measures” could delay the need for a new, higher, limit until early 2013.

Businesses and Wall Street want Washington to fix the issue well before that. Specifically, they want Congress to agree on a lame-duck package that avoids the automatic spending cuts and tax hikes dubbed the “fiscal cliff” and provides a framework for a broader deficit reduction deal next year. At the same time they want to prevent 11th-hour brinksmanship of the sort that triggered a U.S. credit downgrade in the summer of 2011.

Rob Nichols, president and chief executive officer of the Financial Services Forum, told The Hill, “The downside risk here is significant if we don’t include [a debt-ceiling increase with the ongoing fiscal talks]. It’s very sensible to include that, so we don’t roil the global capital markets any further.” Ken Bentsen, head of the Washington office at the Securities Industry and Financial Markets Association, agrees, as does the U.S. Chamber of Commerce.

Remember, we’re not talking about MoveOn.org urging Republicans to be responsible; we’re talking about corporate lobbyists and industries that tend to keep GOP offices on speed dial and are accustomed to having Republicans take their fears seriously.

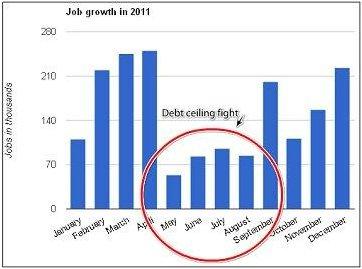

But in this case, Corporate America and Democrats are on the same page, hoping to see a debt-ceiling increase included in any kind of fiscal talks before the end of the year, while far-right GOP lawmakers insist on a replay of the 2011 crisis. Some in Washington may have forgotten this, but the Republicans’ debt-ceiling scandal last year did severe damage to the American economy, depressing job creation, rattling global markets, crushing consumer and investor confidence, and undermining the nation’s reputation and credibility around the globe. When Republicans, for the first time in American history, said they were prepared to trash the full faith and credit of the United States, on purpose, unless non-negotiable demands were met, GOP policymakers hurt the very people they claim to represent and care about most. The “job creators” are urging their allies not to make the same mistake twice. We’ll see soon enough whether Republicans are prepared to listen.

The place for in-depth analysis, commentary and informed perspectives. Recommended