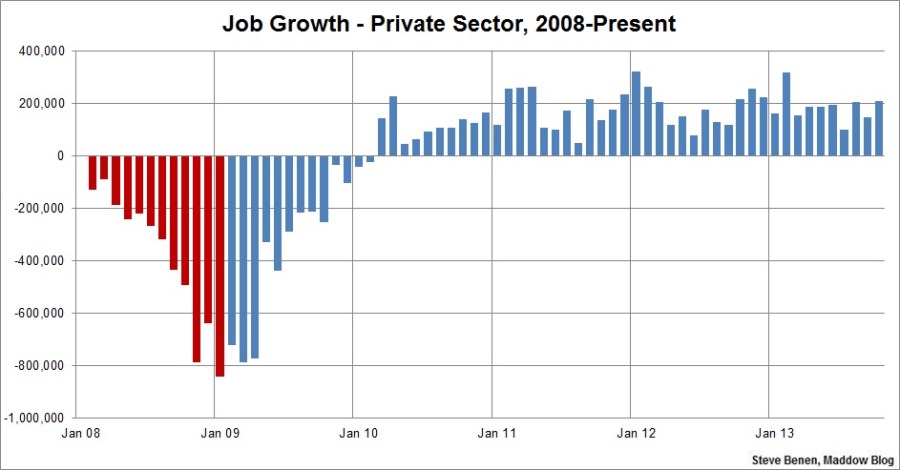

Despite the government shutdown and debt-ceiling fiasco, the economy added more jobs than expected in October. The economy added 204,000 jobs last month, according to the Bureau of Labor Statistics report.

That’s better than the past year, on average, when job growth has averaged 190,000 per month. Revisions also added 60,000 more jobs to August and September. The jobs report suggests that the economy is picking up in spite of everything that Washington has done to get in its way. In terms of payroll numbers, “there were no discernible impacts of the partial federal government shutdown on the estimates of employment, hours, and earnings,” the Bureau of Labor Statistics said.

It’s not all good news, however. The unemployment rate rose slightly from 7.2% to 7.3%, based on a separate survey that counts furloughed workers as “unemployed on temporary layoff.” In fact, the unemployment rate probably should have been higher, as some furloughed workers were misclassified in the survey, BLS says. But even if you discount furloughed workers, the number of employed people overall fell overall. And more are dropping out of the labor force altogether, as the participation rate fell by 0.4 percentage points to 62.8%, which could partly reflect the shutdown hit to consumer confidence.

Still, US stocks went up on Friday in response to the jobs report; the S&P 500 rebounded from its worst hit in 10 weeks to end the week up.

On the whole, while the jobs numbers were better than expected, the labor market still has a long way to go before it approaches anything close to pre-recession levels. “October’s results beat expectations, but expectations were low,” concludes former White House economist Jared Bernstein. The shutdown is still expected to have hurt the economy in other ways. The halt to government activity disrupted private-sector business across the country, slowing growth. While some of that business will be made up for later, not all of it will: Vacations to national parks won’t be rescheduled; crab fishermen lost days in the season they won’t get back. That’s why analysts are expecting a hit to GDP growth this quarter. So the fact that the recovery is continuing despite Washington is a good thing. But it could also be doing even better if Congress stopped sabatoging growth every few months.

Suzy Khimm Recommended

![]()